A homepage promising 0.0 pip spreads, 1:2000 leverage, “no slippage”, “no requotes”, and “no rejections” is, in our experience, less a list of features and more a checklist of red flags that no top-tier regulator would ever allow on a compliant broker’s website. GTCFX combines these claims with impressive numbers — 985,000 clients, 20 destinations worldwide, a $750 billion monthly volume — none of which appear in any audited report we could locate. We wondered whether the substance behind the slogans matches the polish of the marketing, so we pulled up every registry, license number, and warning list we could find to put this broker through a proper review.

GTCFX Quick Card

| Investigation Date | 29/04/2026 |

| Active Website | https://www.gtcfx.com |

| Domain Age | Since 16/06/2015 |

| Brand Name | GTCFX |

| Operating Entity | GTC Global Trade Capital Co. Limited |

| Stated Jurisdiction | Vanuatu, South Africa, UAE, Australia, Mauritius, UK |

| Blacklist Status | Warned by FSA Japan (27/03/2026), NSSMC Ukraine (17/02/2025), SCA UAE (13/04/2023), CB Russia (25/06/2024) |

| License Status | Verified |

| License Number | VFSC 40354, FSCA FSP 51545, FSCM GB22200292, FCA 744501, SCA UAE 20200000007, ASIC AFSL 496371 |

| Office Address | 1/Floor, B&P House, Kumul Highway, Port Vila, Vanuatu |

| Phone Number | +971 800 667788 |

| Support Email | support@gtcfx.com |

| Quick Contacts | Live chat/Messengers/Social profiles |

| Company Activities | Brokerage |

| Investing Terms | $1 |

| Risk Assessment | Average |

Let’s Identify the Company’s Background

GTCFX presents itself as a multi-asset CFD and forex broker offering trading on currencies, metals, indices, energies, and shares, and any company that handles client deposits and routes trades to global markets must, by definition, hold a valid license from a recognized financial regulator. The benchmark here is simple: a legitimate broker is supervised by a tier-1 authority (FCA, ASIC, BaFin, FINMA, CySEC, or equivalent), keeps client funds in segregated accounts at top-tier banks, publishes audited financial statements, and clearly discloses which legal entity the client is actually contracting with.

We’ve already noticed that the GTCFX website piles up an impressive list of regulator logos, but our preliminary check showed that most of them belong to sister entities doing unrelated activities — not to the company that actually accepts your deposit. In the next sections, we’ll walk through every legal entity, every license number, and every registry record to see what’s genuinely backing this broker and what’s just decorative branding. Let’s see whether the substance matches the marketing.

GTCFX Jurisdiction and Regulation

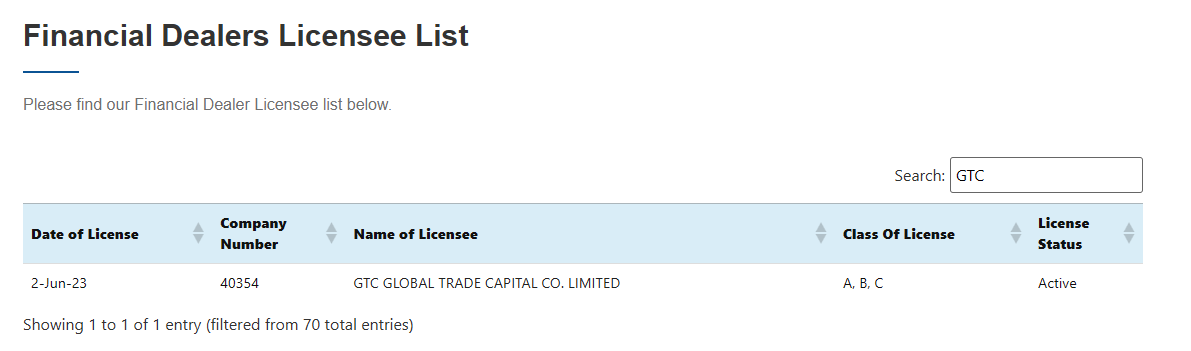

The first thing we noticed on the gtcfx.com website is a textbook example of what regulators call “jurisdictional carve-out“: GTCFX runs not as a single company but as a network of seven legal entities scattered across six jurisdictions, with the actual trading account quietly assigned to the offshore one. The website itself states that when you open an account, your relationship is governed by GTC Global Trade Capital Co. Limited, registered in Vanuatu, under VFSC license No. 40354 — which you can verify directly in the regulator’s public register. Every other logo on the page belongs to a sister entity doing something else entirely. This split-entity model is a deliberate strategy that allows brokers to display impressive regulatory logos while routing real client liability to the weakest link in the chain.

In our opinion, this can hardly be called multi-regulation. In reality, we are dealing with regulatory window-dressing. Once a dispute arises, EU, UK, Australian, or UAE laws don’t apply to your account; your only recourse is Vanuatu, a jurisdiction that is bluntly classified as offering minimal real oversight.

Gtcfx.com History

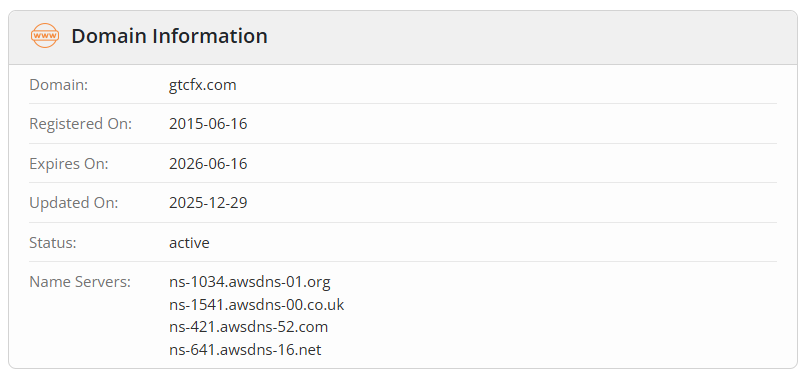

The company claims on its “About” page to have been established in 2012, building a narrative of more than a decade of operational excellence and a client base nearing one million. We decided to cross-check that claim against the only objective record that doesn’t lie — the domain’s WHOIS data.

According to the WHOIS record for gtcfx.com, the domain was first registered on June 16, 2015, not 2012. That’s already a three-year gap between marketing and reality.

Faced with such a glaring gap between the “founded in 2012” claim and a domain that was clearly idle until 2019, we went looking for any predecessor address that could justify the legend. The result was telling: every domain we managed to tie to the GTC brand started operating long after 2012, and none of them carried real broker activity from that year either.

This is a strange situation: the company loudly advertises a 2012 founding date, but not a single domain, not a single legal entity, and not a single archived website page supports that claim. The earliest verifiable artifact of any GTC-branded brokerage activity is the 2017 SCA UAE authorization of GTC Multi Trading DMCC — and even that operated in commodity clearing, not the retail CFD product gtcfx.com sells today. Finally, the current trading counterparty in Vanuatu is less than two years old.

Due Diligence: Onboarding & Funding

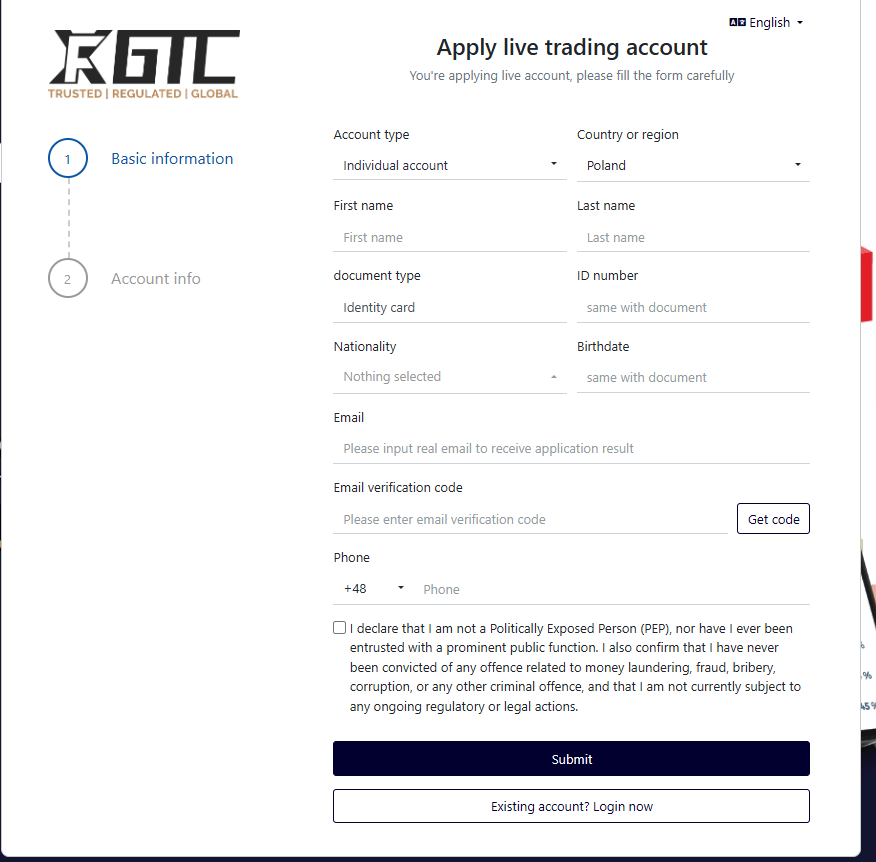

Once we’d finished mapping the regulatory and historical layers, we moved on to the most practical question any prospective client will face: how exactly does the broker bring people in, verify them, and accept their money? In our experience, the onboarding funnel is where offshore brokers either reveal themselves as serious operators or quietly expose the friction-light, KYC-light pipeline typical of high-risk platforms.

The sign-up flow on gtcfx.com consists of a two-step form. The first step asks for a fairly standard set of basic information:

- Account type (Individual/Corporate).

- Country or region.

- First and last name.

- Document type and ID number.

- Nationality and birthdate.

- Email + verification code.

- Phone number.

- A self-declaration checkbox confirming the user is not a Politically Exposed Person and has no AML/fraud convictions.

A few things stood out immediately. There is no two-factor authentication offered at registration, no captcha visible in the captured flow, and no password complexity requirements shown until the second step. The second issue is the PEP/AML declaration mechanism.

GTCFX advertises a fairly broad set of funding rails on its public-facing pages. The deposit and withdrawal methods listed include:

- Credit and debit cards — Visa and MasterCard.

- Bank wire transfer — international SWIFT for larger amounts.

- Digital currency assets — primarily USDT (Tether), both TRC-20 and ERC-20 networks, frequently promoted as the fastest option.

- Local/regional payment processors — referenced on the website but not individually enumerated.

Withdrawals are claimed to be processed within 24 hours internally, with the total time depending on the chosen method (e-wallets and crypto fastest, bank wires taking several business days). The minimum deposit varies by account type: $0 for the Standard account, $5–$50 for the Pro account, and $3,000 for the ECN account. Inactivity fees apply after a dormancy period, although the exact threshold is not clearly documented on the public site.

GTCFX Conditions and Manipulations

The company positions itself as a provider with “direct access to top-tier banks”, “deep liquidity pools”, and “10-millisecond execution”, yet across the entire website not a single liquidity provider is named — no Citi, no JPMorgan, no LMAX, no Currenex, and no Equinix server location. The structural giveaway is the account ladder itself: the Standard and Pro accounts offer zero commission with spreads from 0.9 pips and leverage up to 1:2000, which is a textbook 100% B-Book/Dealing Desk product.

And the most aggressive signal is the trio of guarantees printed on the homepage: “No Slippage”, “No Requotes”, and “No Rejections”. These three promises are technically impossible on any liquidity-routed model — real markets gap, real LPs reject orders during news, and real prices slip during volatility. The only way a broker can promise the absence of all three is by quoting against itself, i.e. running a synthetic price feed inside its own server rather than connecting to anything external. Top-tier regulators specifically forbid this kind of language because it misleads clients about what execution actually means; you will not find it on any FCA, ASIC, or BaFin-licensed broker’s website, for the simple reason that compliance officers would block it before publication.

Gtcfx.com Withdrawal Integrity & Exit Process

There is no dedicated withdrawals page laying out per-method fees, no published cut-off times, no policy on how the broker handles a mismatch between deposit and withdrawal channels (a common point of friction when clients fund by card and try to withdraw to crypto), and no clear explanation of what happens to a remaining balance below the unspecified withdrawal minimum during account closure.

The behavioral evidence from public complaints fills in those blanks in an unflattering way. The recurring scenarios we identified across Trustpilot, WikiFX, and Russian-language review sites cluster around three patterns:

- Threshold gaming — small residual balances are held hostage with newly-invented “minimum” or “activation” deposit demands ($10, then $50) that have no published basis in the T&Cs.

- Server-side blocking — MT5 accounts are flipped to “Trading disabled” without notice, which conveniently freezes equity that would otherwise be withdrawable.

- KYC weaponization at exit — proof-of-source-of-funds, notarized translations, and re-verification requests are introduced after the withdrawal request, never at deposit, and with no consistent timeline for resolution.

Strengths & Weaknesses Analysis

-

Wide instrument coverage across MT4, MT5, and cTrader.

-

The real counterparty is an offshore Vanuatu shell.

-

Flagged by Japan's FSA, the Russian Central Bank, and the UAE's SCA.

-

B-Book conditions disguised as ECN, with prohibited 1:2000 leverage.

-

"Established 2012" claim contradicted by domain and registry data.

-

Documented withdrawal friction with no tier-1 recourse.

Investment Risk Summary

Pulling together everything our GTCFX review has uncovered, we cannot in good conscience call this broker legitimate in any tier-1 sense. In our opinion, the risks here clearly outweigh any short-term convenience, and we would strongly advise choosing a genuinely tier-1-regulated broker instead.

I do not recommend GTCFX! You’ll suffer through pushy account managers and enormous spreads. Oh, and your terminal will constantly freeze on you. So you’re better off finding a different broker. I traded here for a whole year and lost more than $3,400, so I know what I’m talking about!

I’ve been trading through them for about three months now, and the execution quality is frankly poor. On stop-losses, I consistently get hit with slippage of around 15–18 cents in both directions, and it’s always against me. During news releases, the terminal just freezes up and orders sit there unprocessed. It feels like the system is working against the trader rather than with the market — typical dealing desk behavior without any real liquidity providers.